Time is out with its new cover story by Jim Grant, a bow-tie-wearing fellow who runs a publication titled Grant’s Interest Rate Observer.

I am not a fan.

I am not alone.

Why do so many people think this cover and the article that follows it are painfully, unforgivably inane—a limp collection of poorly formed conservative tropes about the dangers of debt? Let us count the reasons.

First, that number—$42,998.12. It’s sort of scary up against that doomy red background. It’s addressed to you. You, dear Publix shopper, idly staring at the checkout lane magazine rack! You, frequent business flyer, killing time in the Hudson News at LaGuardia! It is also a fairly meaningless way to measure the national debt. If we were Botswana, $42,998.12 per man, woman, and child might be a lot of money. But we are not Botswana. We are the United States, a rich, advanced nation with an $18 trillion economy and ample ability to pay the interest that we currently owe our creditors. Stating debt per American tells us nothing whatsoever about whether we have borrowed too much. It is intellectually empty information, a Dorito in stat form.

You might argue that Time is simply trying to personalize what is otherwise an abstract, painfully dry issue.

This brings us to issue No. 2, the subhed: “That’s what every man, woman, and child would need to pay to erase the $13.9 trillion U.S. debt.”

This implies that paying off our national debt might be a necessary or desireable goal. It is neither. We do not need to “erase” the debt. And it would be a horrible idea if we did.1

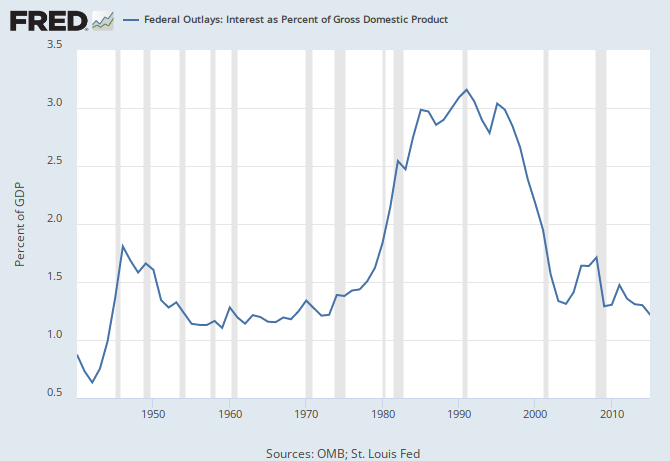

As a rule, it does not matter how much money a country owes if it can easily meet its interest payments. So long as that is the case, bond investors are typically happy to continue lending money, and everything goes smoothly. It’s the same way you or I can carry a mortgage or credit card balance without triggering personal financial catastrophe, and without scaring away our bank. The United States, for its part, has managed to shoulder at least some debt continuously without major incident ever since 1835. And while this may frustrate men like Rand Paul, more rational people should take it as a sign that government borrowing, in and of itself, is not that scary. Currently, interest on the debt only takes up about 6 percent of the federal budget. As a percentage of GDP, it is lower than any time since the 1970s. In the future, we will only have to pay down enough debt to make sure our interest payments remain sustainable, as they are today. We will never have to eliminate the whole balance.

{kind=link}

Doing so would be stunningly foolish anyway. For one, markets would go crazy. The entire financial world runs on Treasury bonds—they are the gold standard of safe assets, and are essentially treated as the next closest thing to cash. Paying them all off would suck the blood out of the world’s financial circulatory system.

Erasing the whole debt, or even a significant chunk of what the U.S. now owes, would also be a waste of resources, especially at a moment when the economy is underperforming its potential.2 Every dollar we spend paying down our obligations could, theoretically, be used on something more productive that would grow the economy long term, like fixing our infrastructure, or making sure we have a functioning health care system. Faster growth would, of course, shrink our debt as a share of the economy. Cutting spending to pay off debt, on the other hand, could slow growth, and leave us right back where we started.

To be sure, sovereign debt can become a problem if investors suddenly decide it looks like a nation might default. This is a grave concern for a country like Greece, which does not control its own currency. Thankfully, in addition to the power to tax, the United States has the near magical ability to print dollars. There is no danger that we will run short of them. Rather, the only potential problem is that one day, we will print so much of our currency that it will create excessive inflation, our debts will become worthless, and the bond markets will strike.

This is basically what Grant seems to think will happen. He does not actually appear to think we need to pay down the whole debt. But he does think we are currently on the road to financial perdition:

We owe more than we can easily repay. We spend too much and borrow too much. Worse, we promise too much. We conjure dollar bills by the trillions–pull them right out of thin air. I won’t insist that this can’t go on, because it has. I only say that it will eventually stop.

I don’t know the date, but I believe that I know the reason. It will stop when the world loses confidence in the dollars we owe. Come that moment of truth, the nation will resemble Chicago, a once prosperous polity now trying to persuade its once trusting creditors that it is actually solvent.

The nice thing about qualifying your sweeping prediction with “I don’t know the date” is that your statement is completely unfalsifiable. (It is also not really a prediction.) In the meantime, very few people with money on the line seem to agree with Jim Grant. The U.S. can currently borrow money for 20 years at historically low rates. Grant cautions that, one day, rates may rise, and the U.S. will have to refinance its debts at higher rates. (“At 4.8%, the rate prevailing as recently as 2007, the government would pay more in interest expense–$654 billion–than it does for national defense,” he notes.) This is a possibility, sure, though right now the world appears to be indefinitely stuck in a low-interest rate trap. Rising health care costs could also potentially force us to borrow a slightly uncomfortable amount in 30 years, though projecting trends that far out is always a guessing game. In the meantime, shooting ourselves in the foot now to address those far-off concerns does not seem like an optimal strategy. Grant’s preferred policy course, a barely coherent combination of a flat tax and massive spending cuts, is especially dubious, and gives one the impression that maybe his debt fearmongering is just pretext for his archconservative preferences about government.

This all brings us to the third issue, the cover’s tag line, and Grant’s “credo,” as he calls it—”Make America Solvent Again.” A company, or a person, is technically insolvent when debts outstrip assets. More colloquially, you’ll hear someone is insolvent when his or her debts are so onerous they can’t possibly be paid. The federal government is not insolvent. Not now. Not any time soon. Saying otherwise is, again, inane.

1Let us pretend, for just a moment, that the United States did decide, on a lark, to pay off its debt. We rely on progressive taxation in this country. The rich pay more. The middle class pays less. You, personally, will not be paying $42,998.12. Nor will your toddler. This is a small point, but worth noting.

2 This might be a different story if anybody was worried about government crowd-out—where rising public debt forces up interest rates and slows down both borrowing and the economy. It has been a long, long time since anybody was concerned about that.