Update, June 25, 10:36 a.m.: The Supreme Court Thursday morning upheld the Affordable Care Act subsidies in a huge victory for the Obama administration. Some 6.4 million people will keep their tax credits. Here’s what else was at stake in the decision:

Once again the fate of the Affordable Care Act rests in the hands of the Supreme Court. In King v. Burwell, the court is weighing whether the federal government can legally provide insurance subsidies to people who have purchased their health care through one of the federally run exchanges in 34 states. Whatever the court decides could also theoretically extend to three other exchanges—in Nevada, New Mexico, and Oregon—that are state-based but federally supported. Altogether, roughly $1.7 billion in tax credits and the health insurance of more than 6 million people is at stake. It’s arguably the biggest existential challenge to Obama’s signature health care reform since the Supreme Court upheld the individual mandate in 2012.

The crux of the case is a perilous clause buried in the ACA’s hundreds of pages. According to the law’s exact wording, people become eligible for federal insurance subsidies if they’ve purchased care through “an Exchange established by the State.” Because of those last four words, the plaintiffs in King v. Burwell argue that federal subsidies can only be available on state-based exchanges, and not on the federally facilitated ones in most of the country. The Obama administration has countered that the purpose of the law is to make health care accessible, and that “established by the State” should be read with that in mind. Several of the people who helped pen the legislation have dismissed the clause as a drafting error.

Whether a key component of Obamacare will fall over that technicality is up to the Supreme Court, which could hand down its ruling as early as Thursday. Until then, here’s what you need to know about the scale of the potential fallout if the subsidies are struck down.

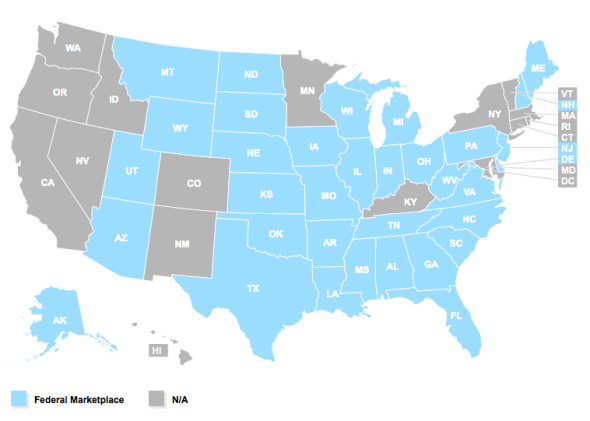

In 34 states (shown in blue below), the health insurance marketplaces are federally facilitated. People receiving subsidies make up 87 percent of enrollees in those states.

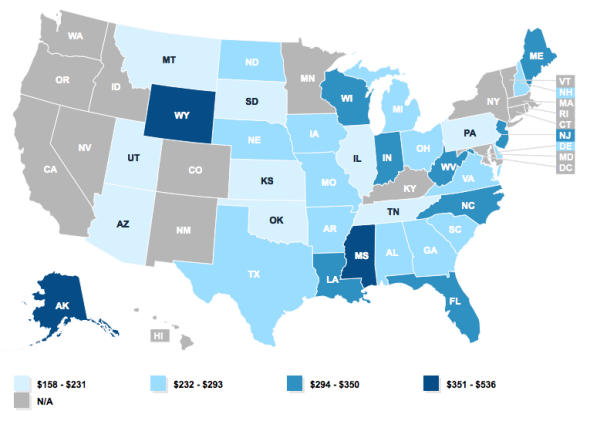

Nationwide, the average person receives $268 per month in government support for their health care, or roughly 72 percent of their premium. But in some states that average is much higher.

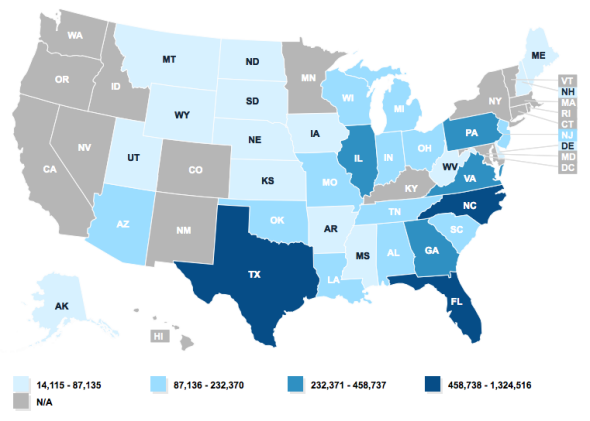

Across the country, some 6.4 million people risk losing their tax credits. On a state-by-state basis, the populations in Texas, Florida, and North Carolina would be hit particularly hard.

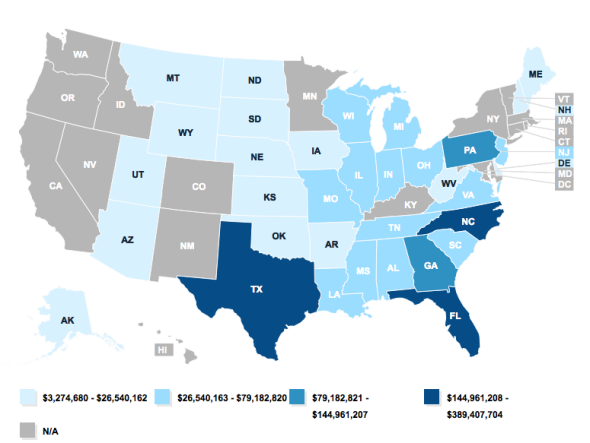

In dollars, that translates to a total loss of roughly $1.7 billion, with the most at risk in Texas, Florida, and North Carolina.

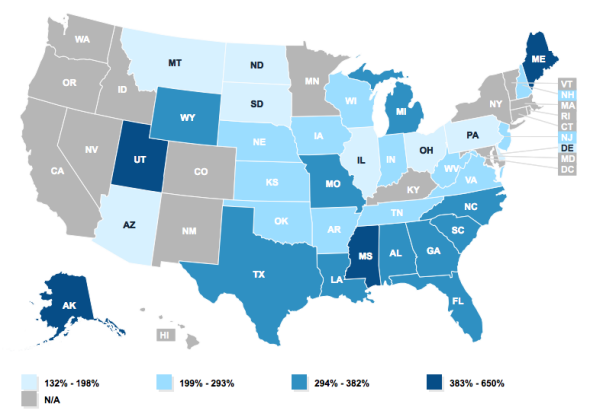

Without the subsidies, out-of-pocket premiums would rise an average of 256 percent for those millions of people. And again, in certain states, the average increase would be greater even than that.

There are a lot of things to be worried about should that happen. For starters, most of the people who lost their subsidies would likely find themselves unable to afford health care. That would drive many of them—especially the young and healthy ones—out of the marketplace. The people who chose to stick around would overwhelmingly be the sicker ones, who relied heavily on insurance to cover their medical expenses. (The individual mandate wouldn’t stop this exodus because the vast majority of people receiving subsidies are exempt from paying it based on their income.) So the entire pool of enrollees would shrink, with the balance tipping toward sick individuals with higher costs. To accommodate that, insurers would probably be forced to raise their premiums—driving out more young, healthy, and cost-sensitive people, and triggering what’s commonly known as the “death spiral.”

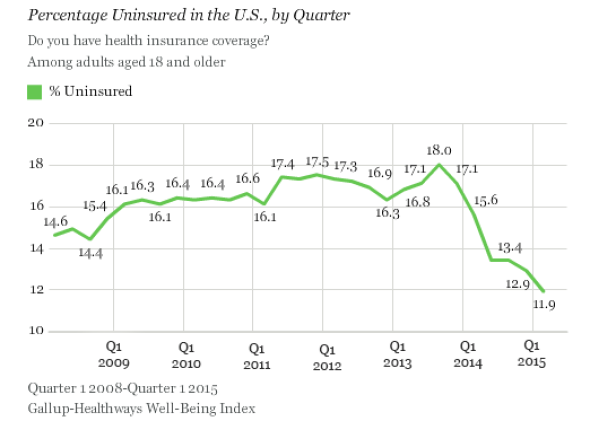

Anyway, you get the picture. A lot of people could lose their health care. That could force a lot more people who before might have been able to afford their health care to drop it as well. And that beautiful decline in the uninsured rate that Gallup has recorded over the past two years? That would probably be wiped out too.