The millennials aren’t saving any money. I mean, a few twentysomethings might be stuffing some crinkly dollar bills under their futons or something, but in aggregate, we’re burning more cash than we’re putting away. Earlier this week the Wall Street Journal reported that following “a flirtation with thrift after the recession,” the personal savings rate of Americans under the age of 35 has dipped to -1.8 percent. The median net worth of young households has also plummeted since the recession.

This news has, of course, led to both shrieking and thumb-sucking. “Millennials Face a Savings Time Bomb,” CBS declared in a follow-up story. (Our empty checking accounts are apparently incendiary devices now.) The Atlantic, taking a turn into econo-cultural analysis, suggested that “the fact that Millennials are more skeptical than ever of banks” might have something to do with our spendthrift ways.

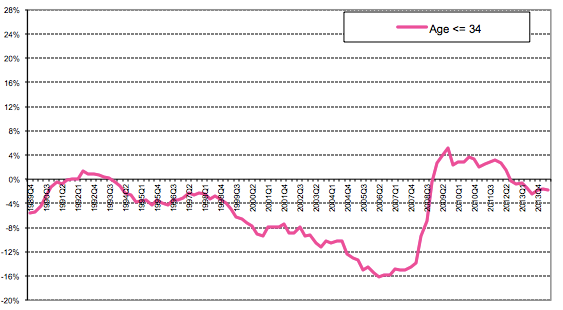

It is true that millennials are probably in worse financial shape than Gen X or the Boomers were at their age. We have far more student debt than any generation before, which has cut into our wealth, and we graduated into a blasted moonscape of a job market (although, to be fair, the early 1980s weren’t exactly a fun time to enter the workforce, either). But I think something should be made clear here: Young adults have never been good at saving, and they are no worse at it today than 15 or 20 years ago. For the past quarter-century, in fact, a negative savings rate seems to have been the norm for the under-35 set, as shown on the graph below, based on the same Moody’s Analytics data the WSJ used for its story. (It’s a bit hard to read—sorry—but the chart stretches back to 1989.)

Moody’s Analytics

This shouldn’t be surprising. Young people don’t make a great deal of money. But they are busy buying their first cars and first homes, and having their first children. At least, they typically are during good economic times. It’s worth noting that the last time the young adult savings rate turned positive, according to Moody’s, was during the rough patch of the early 1990s. I don’t think the reason for that was that the savings and loan crisis made Gen Xers distrust the financial industry. Rather, when the labor market gets choppy, young people put away their credit cards and are less likely to make big life purchases.

So the problem for millennials doesn’t appear to be that we’re frightened of JPMorgan or comfortable putting away an unusually small share of our income. It’s that we’ve gotten a start in life at an inopportune moment in history, and probably have lower salaries and higher education debt to show for it. We’re not bad savers by American standards. But American standards might not be good enough, at least if any of us ever want to retire.