This story originally appeared in Medium.

Default: It’s the worst thing that any debtor can do. It marks you out as being a deadbeat, unable or unwilling to keep your promises. And it’s particularly bad if the debtor in question is a sovereign nation, because the taint of default adheres not only to the government of the day but also to future governments, as well as everybody in the country. Any present-day company or individual who needs to borrow money will find it impossible, or at least much harder, if their government is in default.

I vividly remember an article I read when I first started out in financial journalism, in the mid-1990s, saying that no sovereign borrower had ever defaulted on a Eurobond issue. That article stuck with me in the run-up to Ecuador’s default, in 1999, which I covered in great detail for Bridge News. Ecuador was a small country, and a serial defaulter, but its default was still very big news and had significant repercussions for the sovereign debt markets as a whole.

Certainly Ecuador’s default was a very big deal for Ecuador: The government fell, the country’s recession worsened, inflation soared, and the Ecuadorean currency, the sucre, just disappeared entirely. The default was both symptom and cause of a major national crisis. None of this was surprising to anybody: A bond default is the worst kind of default, for any country. If you default on a bank loan, that’s the bank’s problem. If you default on a bilateral loan from a formerly friendly country, that’s the Paris Club’s problem. But if you default on a government bond — especially if that bond is partially guaranteed by the U.S. Treasury — then that’s much worse: It affects everybody.

That worldview is deeply embedded in a quote from the New York Times on Wednesday:

“Default cannot be allowed to lapse into a permanent condition,” said Daniel A. Pollack, the lawyer that Judge Griesa appointed to oversee negotiations between Argentina and the holdouts. “Or the Republic of Argentina and the bondholders, both exchange and holdouts, will suffer increasingly grievous harm, and the ordinary Argentine citizen will be the real and ultimate victim.”

The fact that Pollack is being quoted in the Times at all is quite astonishing. His job is to be the behind-the-scenes mediator, shuttling back and forth between Argentina and its holdout creditors, in highly confidential negotiations. His job is not to start spouting off to the Times about whether or not default can “be allowed to lapse into a permanent condition” — as though there is some authority who has the ability to allow or not allow such a thing.

But it’s easy to see why Pollack feels comfortable saying such things to the Times: He thinks he’s saying something so banal as to be substance-free. I’m sure that both sides have told him exactly the same thing — this is one of the few areas where they can actually agree!

If so, Pollack should start boning up on the difference between what people say, and what they actually believe. For the fact is that what we’re seeing in Argentina right now is not a typical bond default. As a result, it is not having typical bond-default consequences.

The exchange bondholders are not suffering grievous harm: Nearly all of them are quite happy right now, having bought their bonds well below the levels at which they’re currently trading. The holdouts are not suffering grievous harm: They bought nonperforming debt, they still own nonperforming debt, and the value of that debt is much higher than what they paid for it. And as for the ordinary Argentine citizen, well, there’s a lot of inflation and unemployment and black-market foreign-exchange trading going on, but that’s been true for years, and it’s far from clear how much — or even whether — the default is going to exacerbate such things.

Indeed, Argentina is in pretty good financial shape right now. Both the country and its corporations have relatively little debt, which means relatively little problem rolling it over. Bank deposits are stable. The exchange rate doesn’t seem any more fragile than it has been for months. Foreign reserves have actually been going up in recent weeks. In terms of day-to-day financial life in Argentina, today looks almost identical to yesterday. Nothing much has really changed.

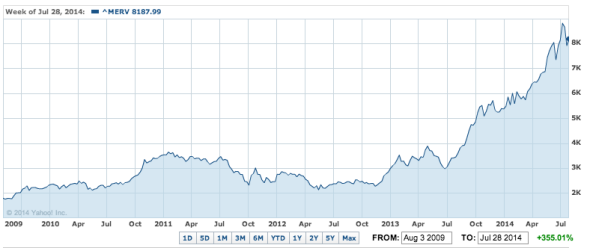

Or, just look at the Argentine stock market —the chart at the top of this article. You’ll see that it’s been on a veritable tear. Part of that is just inflation — but part of it is the market showing that it doesn’t particularly mind the fact that the sovereign is back in default.

Just like anything else, the more common something becomes, the less of a big deal it becomes. And in the wake of the financial crisis, everybody knows that all credit is risky — even sovereign EU credit, like that of Greece. Even, for that matter, the safest credit in the world. After all, there’s a case to be made that the USA defaulted on its sovereign obligations last year. If America can default without the world coming to an end, it should hardly be surprising that Argentina can do the same.

Argentina’s stocks did fall sharply on Thursday— more than 8 percent on the day. Even U.S. stocks fell more than 3 percent. But it’s hard to tell how much of either move is attributable to the default, and in any case both markets remain near their historical highs.

Indeed, one possible lesson from Argentina’s default is that maybe a single day of stock-market volatility could actually turn out to be the worst thing that’s going to happen. Listening to finance minister Axel Kicillof raging against the evil vulture funds, it’s hard to imagine that the country will come to a settlement with its holdout creditors any time soon. Not this year, I’m fairly sure, and probably not until after a new president is elected in October 2015.

If Kicillof becomes the next president (stranger things have happened, in Argentina), then we might indeed end up in Pollack’s worst of all possible worlds, where default becomes a newly permanent condition. Just as it was between 2001 and 2005. Argentina survived those years, during which its government was very popular.

Argentina has done a very good job of not blinking, so far, in the face of U.S. courts threatening the worst possible consequences. The day of reckoning has now arrived, and the consequences are going to be suffered. Many observers might end up being quite surprised at how easily Argentina ends up weathering them.